Economy

Economy

Việt Nam, Czech Republic step up local investment, trade cooperation

1.

|

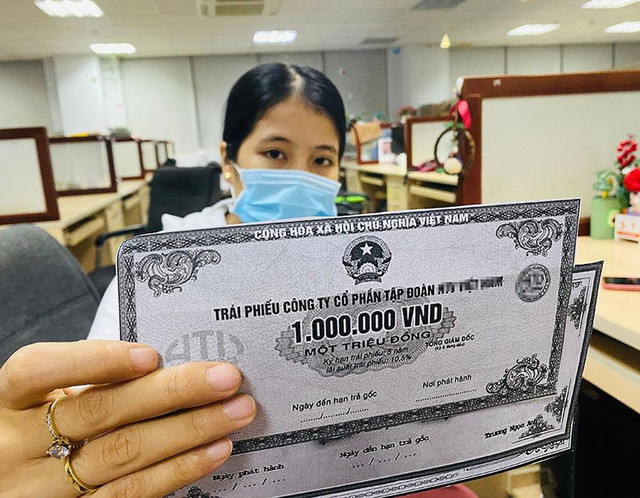

| Over $7.68 billion worth of corporate bonds, equivalent to about 14 per cent of the outstanding corporate bond stock, will mature in 2026. — Photo vtv |

HÀ NỘI — As the corporate bond market continues to recover from a period of heightened defaults and deferred payments, 2026 is emerging as a pivotal year for both issuers and investors.

Market data indicate that a concentrated wave of redemptions is set to place significant pressure on a segment of bonds already flagged as problematic.

Industry analysts point to a backlog of bonds issued in 2023 and 2024 that were slow to repay principal and interest.

Many of these had their maturities extended by two years under Decree 08/2023/ND-CP, a Government measure designed to give issuers additional time to address liquidity constraints. This extension has shifted the centre of redemption risk squarely into 2026.

Estimates from ratings agency VIS Rating show that more than VNĐ200 trillion (US$7.68 billion) worth of corporate bonds, equivalent to around 14 per cent of total outstanding corporate bonds, will mature in 2026. The real estate sector accounts for more than half of this amount.

Among the largest issuers facing redemption obligations are several property developers with multi-trillion-đồng bond packages falling due this year.

Notable examples include Van Truong Phat Construction and Investment Corporation with about VNĐ10 trillion, Hai Dang Real Estate Development Investment and Co. with VNĐ6.65 trillion and Truong Minh Real Estate Investment and Development Co. with VNĐ5.5 trillion. TIZCO JSC and R&H Group are also facing substantial maturities.

Of these, R&H Group stands out due to both its scale and its history of payment difficulties. In 2025, R&H repeatedly sought extensions for interest payments on two bond tranches, identified as RHGCH2124005 and RHGCH2124006, with a combined face value of roughly VNĐ5 trillion, citing prolonged financial strain and limited available liquidity.

The most recent publicly disclosed financial statements for these issuers date back to 2023, showing R&H with total liabilities of nearly VNĐ8.4 trillion and accumulated losses exceeding VNĐ1.12 trillion. Links with other listed entities also point to interconnected risk exposure within the private credit market.

Despite the concentration of upcoming redemptions, recent bond market activity suggests shifting dynamics that may partially ease immediate pressure on distressed instruments.

A 2025 market report by Vietcombank Securities showed a rise in issuance, with 578 tranches raising approximately VNĐ645 trillion, up about 45 per cent year on year. Banking sector issuance accounted for 64 per cent of the total, while real estate represented 26 per cent.

Buybacks of bonds before maturity also rose sharply in 2025, surpassing VNĐ310 trillion, an increase of 43 per cent from the previous period.

This trend, led primarily by banks repurchasing their own three- to five-year bonds, has been viewed as part of broader debt restructuring efforts aimed at easing future repayment pressure.

Real estate issuers also bought back bonds, particularly those issued during periods of high interest rates, in an effort to manage outstanding obligations.

While the overall volume of delayed bond payments declined by around 22 per cent compared with the previous year, non-performing bonds remain heavily concentrated in the property sector, traditionally one of the more volatile segments of the corporate credit market.

In proportional terms, bonds in arrears accounted for roughly 14 per cent of the total problematic stock in 2025.

Vietcombank Securities noted that although 2025 appeared to bring some relief in redemption pressure due to restructuring efforts, much of that burden has effectively been deferred to the 2026-28 period. The apparent easing may therefore represent a shift in timing rather than a fundamental improvement in underlying financial conditions. — BIZHUB/VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

.jpg) Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy