Economy

Economy

Việt Nam bridges interests, strengthens ASEAN solidarity: Indonesian scholar

1.

Moody’s Investors Service on Friday upgraded the Government of Việt Nam’s long-term issuer and senior unsecured ratings to Ba3 from B1 and changed the outlook to stable from positive.

|

| Moody’s Investors Service on Friday upgraded the Government of Việt Nam’s long-term issuer and senior unsecured ratings to Ba3 from B1. — VNA/VNS Photo |

HÀ NỘI — Moody’s Investors Service on Friday upgraded the Government of Việt Nam’s long-term issuer and senior unsecured ratings to Ba3 from B1 and changed the outlook to stable from positive.

“The upgrade to Ba3 is underpinned by strong growth potential, supported by increasingly efficient use of labor and capital in the economy. A long average maturity of government debt and a diminishing reliance on foreign-currency debt point to a stable and gradually moderating government debt burden, particularly if strong growth is sustained over time. The structure of Vietnam’s government debt also limits susceptibility to financial shocks. The upgrade also reflects improvements in the health of the banking sector that Moody’s expects to be maintained, albeit from relatively weak levels,” Moody’s said in a statement released on its website.

According to Moody’s, the stable outlook reflects balanced risks at the Ba3 rating level.

"While downsides may arise from persisting weaknesses in the banking system or if the ongoing trade dispute between the US and China resulted in a sharp slowdown in global trade, there are upside risks from further improvements in debt affordability and better trade performance than we currently project," it said.

Moody’s has also raised Việt Nam’s long-term foreign currency (FC) bond ceiling to Ba1 from Ba2 and its long-term FC deposit ceiling to B1 from B2. The short-term FC bond and deposit ceilings remain unchanged at Not Prime. Việt Nam’s local currency bond and deposit ceilings remain unchanged at Baa3.

Moody’s estimates that Việt Nam’s growth potential is strong, at around 6.5 per cent, supported by increasingly efficient use of labour and capital in the economy. Globally, strong growth potential tends to be associated with relatively low competitiveness. However, Việt Nam’s economic strength combines high growth and high competitiveness as shown in the economy’s ongoing shift towards high value-added sectors.

With an average GDP growth rate of over 6 per cent over the past decade, Việt Nam has climbed up the manufacturing value chain within a short span of time, gaining competitiveness in the assembly of higher value-added electronic products - such as smartphones - while continuing to retain its comparative advantage in the export of labor-intensive goods, such as textiles and garments. Rising competitiveness and a further transition towards higher-value-added industrial activity will support growth at high levels in the medium term. Moody’s projects GDP growth of 6.4 per cent in 2018-2022, higher than the median for B1-rated sovereigns at 3.7 per cent, and Ba-rated sovereigns at 3.5 per cent.

Potential growth is supported by strong investment, including Foreign Direct Investment in high-value-added manufacturing. As Việt Nam continues to move up the value-chain and the contribution of the private sector to total value-added grows, Moody’s expects productivity growth to drive the economy’s growth potential.

Moreover, according to the World Economic Forum’s Global Competitiveness Index, Việt Nam is much more competitive than most other Ba-rated or B-rated sovereigns. Moody’s expects Việt Nam to retain relatively high competitiveness as the shift up the value chain gives room for relatively rapid income and wage increases.

One factor weighing on Việt Nam’s economic strength is the economy’s reliance on credit. Demographic trends, including a sizeable share of working age population-- with relatively higher spending power - in the overall population, and increasing urbanisation have contributed to strong consumption and credit growth. Corporate debt is also relatively high and has been rising in recent years. Previous periods of rapid credit growth have weakened bank solvency and raised contingency risks for the sovereign.

While Moody’s estimates that credit allocation has improved somewhat and poses lower risks to the sovereign, rapid credit growth sustained beyond the pace warranted by financial deepening trends raises the risk of a correction that would amplify the negative impact of an economic shock. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

.jpg) Economy

Economy

Economy

Economy

Economy

Economy

The Ministry of Planning and Investment has co-ordinated with various other ministries and agencies to create a programme to connect the country’s innovation networks.

Economy

Economy

Novaland Group will continue to spend 80 per cent of its resources on developing housing projects.

Economy

Economy

The HCM City real estate market will be positive from now until the Lunar New Year in early 2019, according to HCM City Real Estate Association.

Economy

Economy

Saigon Co-op, the country’s leading fast-moving consumer goods retailer on August 10 opened a new Co.opmart supermarket in Tây Ninh Province’s Gò Dầu town, the 98th Co.opmart store in the country and fourth in the province.

Economy

Economy

The 13th International Exhibition on Products and Supplies for Medical, Pharmaceutical, Hospital and Rehabilitation (Pharmed and Healthcare Viet Nam 2018) will be held next month in HCM City.

Economy

Economy

Four domestic carriers – Vietnam Airlines, Vietjet, Jetstar Pacific and the Việt Nam Air Services Company (VASCO) reported 26,578 delayed and cancelled flights, or 15 per cent of their total flights, in the first seven months of 2018.

Economy

Economy

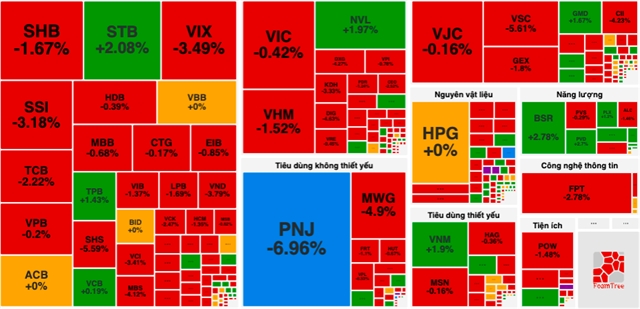

Vietnamese shares ended Friday on a positive note, driven by financial-banking and energy sectors as confidence was boosted by news on State capital divestment from State-owned businesses.

Economy

Economy

The Airport Services Joint Stock Corporation (ASG Corp) has filed to list 34.5 million shares on the HCM Stock Exchange (HOSE).

Economy

Economy

The Government plans not to license any more wholly foreign-owned banks in Việt