Economy

Economy

Keeper of history: Man preserves images of late President, national sovereignty through postage stamps

1.

The The Viet Capital Securities Joint Stock Company (VCSC) has forecast a bleak outlook on sluggish sales and rising input costs for Hậu Giang Pharmaceutical Joint Stock Company (DHG).

|

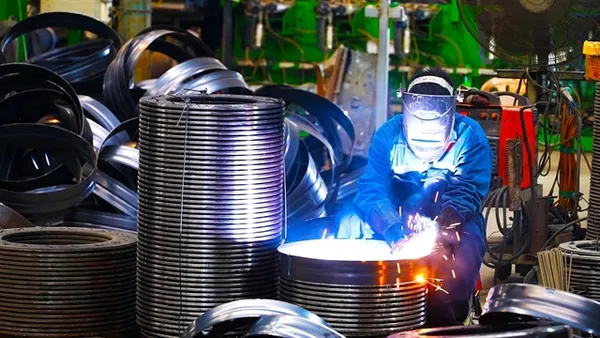

| An automated production line for soft capsules at a factory of Hậu Giang Pharmaceutical Joint Stock Company. — VNA/VNS Photo Hoàng Hải |

HÀ NỘI — The Viet Capital Securities Joint Stock Company (VCSC) has forecast a bleak outlook on sluggish sales and rising input costs for Hậu Giang Pharmaceutical Joint Stock Company (DHG).

The company has downgraded the potential growth of DHG to 'Underperform', VCSC said in its report.

VCSC predicts that the compound annual growth rate (CAGR) of DHG’s after-tax profit in the 2017-2020 period would stand at only 3 per cent per year.

In the first quarter of 2018, DHG’s in-house sales slid 4 per cent year-on-year, VCSC said, adding that amid stiff competition in the over-the-counter (OTC) channel, DHG still lacks distinctiveness in its products.

OTC or over-the-counter means distributing drugs through drugstores.

“We have not seen enough changes in DHG to overcome the headwinds in the OTC channel.”

DHG’s past success was premised on its market-leading distribution network. However, its sales of in-house products have stalled over the last four years as DHG’s distribution coverage has matured, VCSC said.

Its OTC channel, which accounts for 90 per cent of DHG’s sales, is losing its share to hospitals due to the wide coverage of public insurance and domestic pharmacy players, who are intensifying their efforts in the OTC channel, as they struggle to compete against cheaper imported drugs in the hospital bidding process.

“In the coming years, we will see DHG’s in-house sales grow in a low- to mid-single-digit range, bolstered by sales force expansion to provide better services to the pharmacies,” the company said in its report.

Besides this, VCSC said DHG’s in-house products’ gross profit margin (GPM) is poised to contract in 2018, owing to a sharp increase in active pharmaceutical ingredient (API) prices.

The GPM narrowed by 3.1 percentage points year-on-year to 53 per cent in Q1 of 2018. Given DHG’s inventory period of some 3.5 months, we believe the effect of higher API prices will be even more pronounced from Q2 of 2018, given that the rally in Chinese API prices only started in November 2017.

“As such, we project the in-house GPM will reach 51.8 per cent in full-year 2018, down 3.5 percentage points compared to 2017.

In addition to this, DHG has announced its plan to raise its foreign ownership ratio cap from 49 per cent to 100 per cent, which means that the firm will have to stop its pharmaceutical provision to two foreign partners of MSD and Mega.

Another factor negatively affecting DHG’s profit is taxation.

In Q4 of 2017, the tax authority issued a decision on the calculation of DHG’s tax rate, which resulted in a significant upward adjustment in the company’s effective tax rate, VCSC said.

“DHG’s reported tax rate in Q1 of 2018 was not adjusted in accordance with this tax decision, but this will be rectified in H1 2018 financial statements,” VCSC said.

DHG planned to earn a net revenue of more than VND4 trillion (US$175 million), equivalent to the target set for 2017. However, its pre-tax profit is expected to increase by 6.7 per cent to reach VND768 billion.

The revenue from self-manufactured products will account for VND3.5 trillion and grow by more than 13 per cent compared to 2017. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Prosperous business performance and positive bank share price trend in the stock market are expected to help some commercial banks meet capital increase deadline required by the State Bank of Việt Nam (SBV).

Economy

Economy

The Ministry of Industry and Trade (MoIT)’s draft decree on the development and management of traditional markets and supermarkets is facing criticism as it imposes restrictions on retail businesses.

Economy

Economy

Vietnamese shares almost fell to the defensive side on Monday as selling pressure rose in the final minutes of the session and pushed stocks down following recent rallies.

Economy

Economy

The central province of Quảng Trị is getting another wind power plant, thanks to a total investment of US$68 million from a domestic company.

Economy

Economy

The northern province of Thái Nguyên will publish a list of 65 projects calling for investment at the investment promotion conference to be held here on July 1.

Economy

Economy

Russian automotive manufacturer Gorkovsky Avtomobilny Zavod (GAZ) will establish a joint venture to distribute its products in the Vietnamese market after it received good feedback at the Vietnam AutoExpo 2018 held in Hà Nội from June 6-9.

Economy

Economy

The Indonesian Anti-Dumping Committee (KADI) has announced the application of anti-dumping measures on colour-coated steel sheet imports from Việt Nam and China.

Economy

Economy

Under Decision No1250/QĐ-UBND, signed by the committee's chairman Nguyễn Đức Chính on Friday, Quảng Bình Province-located Tân Hoàn Cầu Corporation was allowed to construct Hướng Hiệp 1 wind power plant project in Hướng Hiệp commune, the mountainous district of Đakrong.

Economy

Economy

The first-ever Thanh Hà litchi festival opened in the northern province of Hải Dương on June 10 to promote the local specialty fruit.