Economy

Economy

Sushi Tiger makes its move in Hà Nội

1.

Analyst’s Pick: To cope with constant changes in the global economy and unpredictable events as well as to improve the resilience of the financial market, we need to balance the short-term need for agility and flexibility and the long-term need for stability.

Võ Trí Thành*

|

As we all know, the financial market (including the stock market and bond market, among others) and the financial system (including commercial banks and financial institutions) play a vital role in facilitating the smooth operation of economies by allocating resources and creating liquidity for businesses.

Tasks set for State management agencies are always to both enhance the resilience and ensure the stability of the macroeconomy, while still having to create favourable conditions for these markets to operate smoothly and develop. This is not only necessary for the common course of socio-economic development but also particularly vital for the process of economic recovery this year and in coming years after the economy has been hit hard by the COVID-19 pandemic.

Under the severe impact of the pandemic, the most concerning problems that the Vietnamese financial market has been facing are bad debts – a long-term issue which seems to be exacerbated as enterprises have had to suspend their business and production, and most recently, "loopholes" in financial market, especially in corporate bond market which cause risks to investors and might result in unexpected consequences.

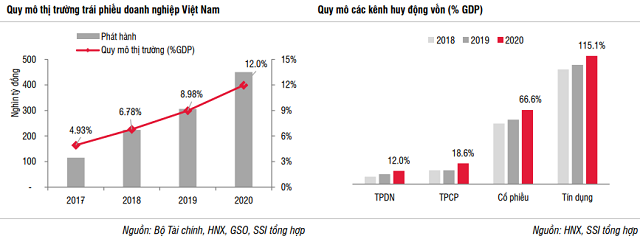

According to the Research and Analysis Department of the Vietnam Association of Realtors (VaRS), the corporate bond market has experienced three to four years of strong development with skyrocketing issuance value. In 2021, the total value of bonds issued reached more than VNĐ700 trillion (US$32.4 billion), equivalent to 16.7 per cent of GDP, accounting for nearly 12 per cent of the country's credit balance.

It is noteworthy that real estate corporate bonds have been booming when investors prioritised using the form of bond issuance to mobilise capital, rather than sourcing capital from banks.

Real estate businesses have surpassed banks, accounting for 35 per cent of the total value of corporate bonds issued in 2021.

In the first three months of this year, the total value of corporate bonds issued reached nearly VNĐ37 trillion, a surge of 47 per cent compared to the same period last year. The proportion of real estate corporate bonds in the period accounted for nearly 60 per cent.

The large proportion of the real estate corporate bonds is attributed to the fact that (i) about 60 per cent of bonds issued will be maturing in 2023-2024 thus demand for capital to pay bond principal and interest is increasing; (ii) commercial banks are tightening credit to property buyers and raising the requirements for lending in the sector.

However, nearly half of the value of real estate corporate bonds is unsecured, according to the VaRS. Having collateral is not required, but it is one of the conditions that create the reputation of the business as well as the corporate bonds that are issued to ensure the safety of bondholders. Meanwhile, credit of enterprises issuing bonds has not been rated by independent and prestigious credit rating agencies and the quality of collateral assets is not ensured.

In addition, the phenomenon of banks selling corporate bonds to individual investors, who do not have enough knowledge and experience to participate in the corporate bond market – which is usually characterised by information asymmetry and only serves professional investors, makes them mistake buying bonds for depositing money at banks.

However, the corporate bond market has been going through a new turning point, with more control and warnings from the State management agencies since the State Securities Commission requested to cancel nine batches of bonds issued by Tân Hoàng Minh Group, with a total value of over VNĐ10 trillion.

In the first half of April, the Prime Minister issued additional documents requesting relevant agencies to correct and stabilise the operation of the corporate bond market, ensuring the market's safe, efficient, healthy and transparent operation.

|

| The combined graphs show the size of the Vietnamese corporate bond market in trillion VNĐ, in comparison to the GDP from 2017 to 2020 (left) and the size of capital mobilisation channels in comparison to GDP from 2018 to 2020 (right) including corporate bonds (TPDN), Government bonds (TPCP), shares (Cổ phiếu) and bank loans (Tín dụng). Source: ssi.gov.vn |

In my opinion, solutions to stabilise the market are indispensable but State authorities’ agility and flexibility are also important in the current context.

To cope with constant changes in the global economy and unpredictable events as well as to improve the resilience of the financial market, we need to balance the short-term need for agility and flexibility and the long-term need for stability.

Personally, I think though the financial and monetary risks are increasing, we are still able to manage the risks to some extent because Vietnamese financial and banking systems are now much more resilient than those of the 1997-98 period when the Asian financial crisis happened and those of the 2010-12 period when the 2008 global financial crisis had taken a toll.

Besides, the country’s macro-economy and macro-indicators are now much more stable. More importantly, policy-makers and managers have been proving to be more proficient in governing the market. This is manifested by the more efficient way the State Bank of Vietnam uses monetary instruments and coordinates monetary policy with fiscal policy to manage money supply, credit and liquidity.

In the short term, especially when the economy and businesses have started regaining momentum for growth, policy changes need to be done step by step to avoid shocks to the market and stakeholders.

For example, it is necessary to follow and assess the potential risks of credit flowing into securities and real estate sectors. But the real estate market has different segments which also have different levels of risk, thus we should not equate the risk levels of all types of properties.

Some real estate projects which have positive spillover effects and are developed based on real demand will likely contribute a large part to economic growth. When dealing with the wrongdoings of real estate investors, State management agencies should consider case by case to impose suitable sanctions rather than letting the whole market be affected.

Compared with other countries in the region such as Malaysia, Singapore, and Thailand, Việt Nam’s corporate bond market size is still very modest. However, in the long run, corporate bonds are still an effective capital mobilisation channel, demonstrating the dynamism of an economy, and giving investors diverse investment opportunities.

Concerns of State management agencies often stem from information asymmetry between enterprises and investors (individuals or organisations). Therefore, the credit rating for bond issuers is extremely necessary. The Government should create conditions for the establishment of independent and professional credit rating agencies. Other fundamental things are to improve the quality of investors (individuals or organisations) and to develop long-term investment institutions such as pension funds and social insurance institutions.

The Ministry of Finance and the State Securities Commission need to set up an effective inspection mechanism for bond issuers from the phase of document submission, instead of detecting wrongdoings after they has successfully made deals, causing unnecessary disturbance to the market.

In medium and long-term, it is important to continue addressing the bad debt issue and restructuring the banking system and stock market. Commercial banks’ renovation should be boosted to meet requirements of best practices such as Basel II and Basel III while the stock market must be upgraded to emerging market level from the current frontier market classification.

*Võ Trí Thành is a former vice-president of the Central Institute for Economic Management (CIEM) and a member of the National Financial and Monetary Policy Advisory Council. The holder of a doctorate in economics from the Australian National University, Thành mainly undertakes research and provides consultation on issues related to macroeconomic policies, trade liberalisation and international economic integration. Other areas of interest include institutional reforms and financial systems.

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

The upgrade of Việt Nam's stock market from frontier to emerging status is a driving force for the future.

Economy

Economy

Economy

Economy

Economy

Economy

Minister of Agriculture and Rural Development Lê Minh Hoan said the Vietnamese agricultural industry needed to take advantage of external forces so as not to be left behind.

Economy

Economy

Economy

Economy

Economy

Economy

Việt Nam enjoyed the largest trade surplus ever, about US$4 billion, in the first four months of this year, 3.2 times higher than the previous year, according to the Ministry of Agriculture and Rural Development (MARD).

Economy

Economy

Việt Nam needs to have an appropriate strategy to promote the development of air logistics and tap its large potential, experts have said.