Economy

Economy

Lâm Đồng races to repair flood damage after days of heavy rain

1.

|

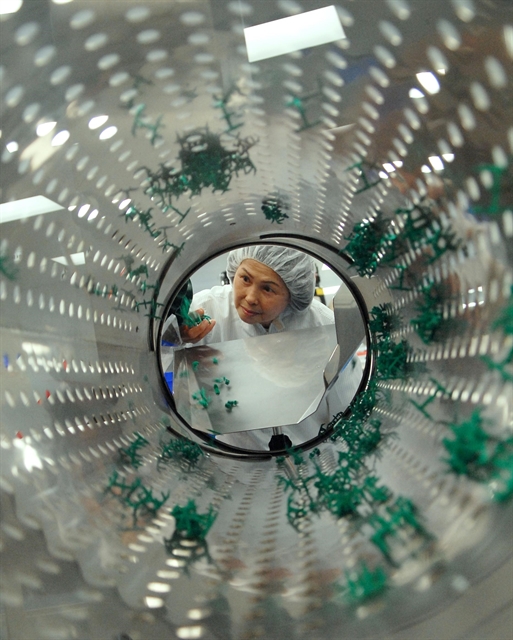

| A bank teller counts cash at a transaction office in Hà Nội. As of September 21, 2023, the credit of the banking system rose by 5.91 per cent compared to the end of 2022 to more than VNĐ12.62 quadrillion. — VNA/VNS Photo |

HÀ NỘI — The bad debt ratio of the banking system skyrocketed from 2 per cent at the beginning of this year to 3.56 per cent, or more than VNĐ440 trillion, at the end of July 2023, according to the latest data from the State Bank of Vietnam (SBV).

Including bad debts that commercial banks sold to the Vietnam Asset Management Company (VAMC) and have not yet been recovered, the bad debt ratio rose to 6.16 per cent.

This bad debt ratio includes the debts of five banks: SCB, Dong A Bank, CBBank, OceanBank, and GPBank, which are under the SBV’s special control. Excluding these five banks, the bad debt ratio stood at 1.92 per cent.

SBV’s Governor Nguyễn Thị Hồng stated that as of September 21, 2023, the outstanding loans of the banking system totalled more than VNĐ12.62 quadrillion, an increase of 5.91 per cent compared to the end of 2022. Notably, the bad debt ratio in the real estate sector rose from 1.8 per cent in July 2022 to 2.58 per cent in July 2023.

The credit quality of many banks has shown signs of deterioration. Some banks listed on the stock exchange, such as NCB, ABBank, BVBank, VPBank, VietBank, OCB, and PGBank, had bad debt ratios exceeding 3 per cent by the end of June 2023.

Experts predict that the credit quality of the banking system may continue to face pressure. Some bank leaders believe the bad debt ratio will peak in the third quarter of this year and start to gradually decrease from the beginning of the next year.

The SBV has highlighted that the domestic and international economic situations are highly volatile due to the escalating Russia-Ukraine conflict, which disrupts the global supply chain. This leads to a rising risk of inflation and impacts the consumer spending of many economies. Việt Nam's major trading partners also face potential recession risks, especially following incidents involving several US banks.

At present, banks' management of bad debts encounters numerous challenges, especially with the rise in overdue debts and a sluggish real estate market, making the handling of real estate collateral even more challenging.

Furthermore, the SBV has noted that the debt trading market still presents many limitations. The legal framework related to restructuring credit institutions and managing bad debts remains incomplete, and there is a lack of favourable policies to encourage both domestic and foreign investors to participate in handling collateral and trading bad debt.

Specifically, the infrastructure of underperforming banks still lacks the resources and specific mechanisms for thorough management. Some State-owned groups and corporations do not have the resources required to manage losses and restructure non-bank credit institutions where they hold ownership or significant shares. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy