Economy

Economy

Fighting against human trafficking

1.

|

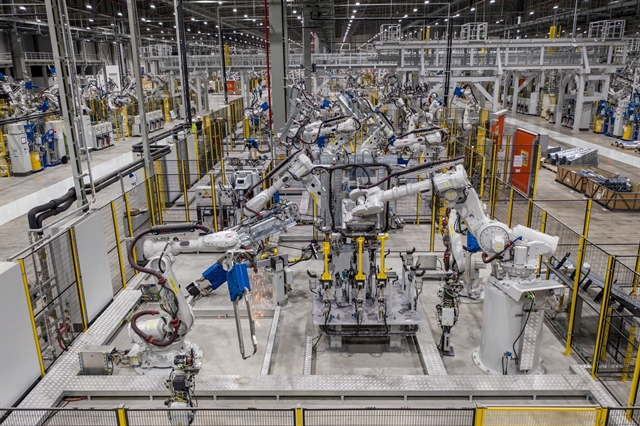

| Rice is packed at Lộc Trời Group's plant in An Giang Province. Lộc Trời Group Joint Stock Company (LTG) recorded a loss after tax of more than VNĐ81 billion (US$3.4 million) in the first quarter, while in the same period in 2022 it reported a profit of VNĐ184 billion. — VNA/VNS Photo Phạm Hậu |

HÀ NỘI The difficult market, coupled with a sharp increase in loan interest expenses, caused the profits of many agriculture enterprises to fall in the first quarter of 2023, with some large corporations even recording heavy losses.

Lộc Trời Group Joint Stock Company (LTG) recorded a loss after tax of more than VNĐ81 billion (US$3.4 million) in the first quarter, while in the same period in 2022 it reported a profit of VNĐ184 billion. However, the group recorded consolidated net revenue up by 4.56 per cent to reach VNĐ2.45 trillion.

Explaining the sharp decrease in profit in the first quarter of 2023, Nguyễn Duy Thuận, General Director of Lộc Trời Group, said that although net revenue increased, the rise in loan interest expenses caused the profit of this business to fall strongly.

In the first quarter of 2023, Lộc Trời recorded an exchange rate difference loss of more than VNĐ17 billion; loan interest expense increased nearly 3 times, to VNĐ105.5 billion, while in the same period last year, it was only VNĐ38 billion.

As of March 31, 2023, Lộc Trời has borrowed short-term loans from banks of more than VNĐ6.2 trillion and nearly US$105 million; in which, the majority were loans arising in the fourth quarter of 2022 and early this year, under the form of unsecured loans, with interest rates ranging from 6 to 9.5 per cent. Notably, there were some short-term loans with interest rates up to even 11 per cent to 12.28 per cent.

They included a loan of more than VNĐ211 billion at Vietnam Prosperity Commercial Joint Stock Bank with an interest rate of 10.5-11 per cent; a loan of more than VNĐ430 billion at HCM City Development Commercial Joint Stock Bank with an interest rate of 11.3 per cent; a loan of nearly VNĐ500 billion at Tiên Phong Commercial Joint Stock Bank with an interest rate of 10.5-11 per cent.

Although over time, the deposit interest rates have been pushed up, the above short-term lending interest rates in VNĐ are too high for an agriculture enterprise. On the other hand, agriculture is one of the five priority areas in the credit policy of the State Bank. According to current regulations, the maximum interest rate for short-term loans in VNĐ for a priority sector is only 5.5 per cent per year.

In the first quarter of this year, Dabaco Vietnam Group Joint Stock Company (DBC), a leading company in livestock production, also recorded a record loss of VNĐ321 billion. The big loss was due to a decrease in revenue, and a sharp increase in loan interest expenses.

According to Dabaco's explanation, the agriculture industry and the livestock industry faced many difficulties due to epidemics in cattle, especially African swine fever, which continued to recur. In addition, the cost of raising livestock increased while purchasing power fell, and the selling price of products in the market remained low for a long time, leading to a sharp decrease in the results of livestock production of subsidiaries.

Not only burdened with interest expenses, some agricultural export enterprises also had to burden additional losses due to exchange rate differences in the first quarter of this year.

Vĩnh Hoàn Joint Stock Company (VHC), the industry leader in pangasius production and export, also recorded poor business results in the first quarter of 2023.

Exports to key markets dropped sharply, while financial expenses increased sharply by 113 per cent, making Vĩnh Hoàn pre-tax profit only reach VNĐ260 billion, down 61 per cent over the same period of 2022.

Vĩnh Hoàn recorded interest expenses of more than VNĐ37 billion, up nearly 95 per cent; exchange rate loss was more than VNĐ45 billion, up 165 per cent year-on-year.

Lacking capital

The problem of Dabaco above is also the general situation of livestock enterprises in recent times. In his letter to the Governor of the State Bank of Việt Nam at the end of March 2023, Nguyễn Trí Công, Chairman of the Đồng Nai Livestock Association, said that domestic companies, farms and households were facing fierce competition from FDI companies with abundant capital.

According to Công, the price of livestock has increased, but the selling price is low, causing a lot of people and livestock enterprises to suffer heavy losses.

At a conference held in HCM City recently, Nguyên Ngọc Nam, Chairman of the Việt Nam Food Association (VFA), said that the community of rice exporters in the Mekong Delta region was now most interested in credit capital.

According to Nam, almost all traders are facing many difficulties in accessing credit capital. However, a low credit limit makes the merchant's purchasing progress significantly affected.

During the main harvest season, rice purchasing faced many difficulties because the bank can not actively open more credit lines for rice exporters.

Nguyễn Hoài Nam, Deputy General Secretary of the Việt Nam Association of Seafood Exporters and Producers (VASEP) said that export processing enterprises in the industry are facing many difficulties in terms of markets, raw materials, credit and production.

Currently, export orders and prices have plummeted, the risk of losing customers, and inventory increases; Meanwhile, the cash flow is limited and interrupted, putting pressure on maintaining the purchase of raw materials and paying the due loans to the bank, he said.

Besides, bank interest rates have increased, especially US dollar loan interest. In previous years US dollar loan interest was only from 2.4 per cent, now it is 4.2-4.9 per cent. Seafood enterprises mainly borrow US dollars.

Therefore, businesses recommended the banking industry have a plan to stabilise the interest rates in certain terms; have separate regulatory policies for agricultural enterprises in order to support enterprises to maintain stable production and business activities.

At the same time, banks need to review procedures and consider having special preferential credit packages for farmers to avoid the circumstances in which farmers have to borrow loans with extremely high interest rates from outside due to inability to access loans from banks. VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy