Economy

Economy

Six Filipinos detained over card-game scams targeting tourists

1.

|

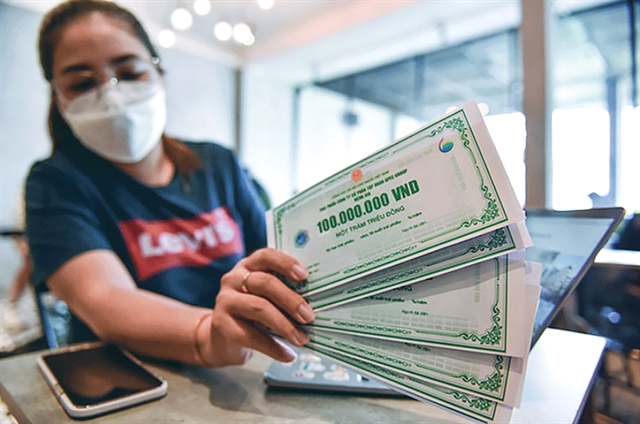

| The State Bank of Việt Nam has announced consultation on a draft circular amending and supplementing Circular No.52/2018/TT-NHNN on credit ratings. VCCI has put forward some proposals in response. — Photo vneconomy.vn |

HÀ NỘI— In cases where banks disagree with the credit assessment of banking authorities, they should be allowed to ask for clarifications on the credit ratings assigned to them, according to the Vietnam Chamber of Commerce and Industry (VCCI) in response to a draft circular amending and supplementing credit rating assessments.

According to VCCI, credit scores are crucial to credit institutions because low-scores are more likely to be inspected and closely supervised by banking authorities. For this reason, banks should be allowed to file complaints when they disagree with the credit results, and the authorities have to respond to the complaints and clarify their assessments.

Thus far no regulations have been introduced to regulate complaints, settlement of complaints and time frames to respond to complaints in regard to credit ratings. Such regulations, if put in place, would add more transparency to assessments and incur no additional administrative costs.

The VCCI believes foreign bank branches should be allowed to provide the results to their parent banks on condition the results be kept secret.

“Such an amendment to Article 23 is reasonable and would not affect the banking authorities as well as other credit institutions,” according to the chamber of commerce and industry.

Under the draft circular, credit institutions and foreign bank branches shall be classified into five credit levels: A (excellent), B (good), C (average), D (fair) and E (poor). This classification is based on the CAMELS rating system that has been accepted by many countries worldwide.

However, VCCI said the five-level system was ineffective as they were not good indicators of bank performances. Many banks with huge performance differences had ended up in the same credit level.

For instance, banks are ranked B if their total score is less than 4.5 and greater than or equal to 3.5. This means banks with 4.4 score and banks with 3.5 score are treated equally.

In fact, the credit risk gap between a 4.4-score banks and 3.5-score bank is huge. Therefore, sub-levels are needed to assess credit institutions properly.

“Each credit level should be divided into sub-levels based on different credit scores in order to better classify credit institutions,” VCCI said. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

The Directorate of Fisheries forecasts a shortage of raw materials for export basa processing in the first quarter of 2022 due to the impact of COVID-19.

Economy

Economy

Economy

Economy

Analysts from securities companies are optimistic about stock market movements during the last trading week of this year and betting that the cash flow will soon shift to good fundamental large-cap stocks like banking and securities groups.

Economy

Economy

Việt Nam's target of bringing its GDP growth to 6-6.5 per cent in 2022 as set in the recent session of the National Assembly is entirely possible if it can effectively control the COVID-19, and improve the supply – demand balance, an official of the World Bank (WB) has said.

Economy

Economy

Vietnamese automaker VinFast on Saturday delivered its first smart electric cars VF e34 to customers, making Việt Nam one of a few countries worldwide mastering electric vehicle production technology.

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy