Talking Shop

Talking Shop

Thailand, Lithuania forge closer ties in historic ministerial visit

1.

|

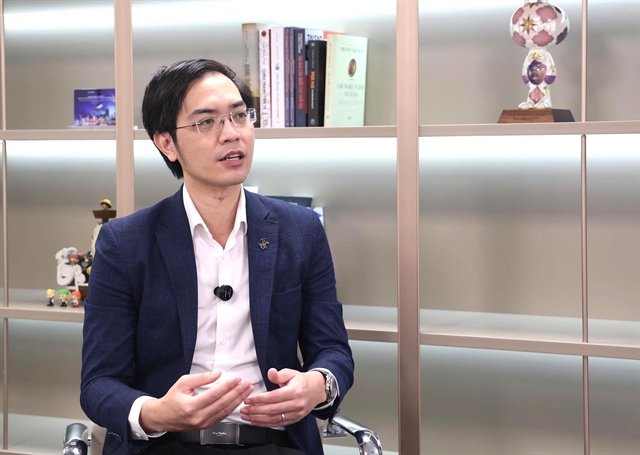

| Mr. Bae Seung Jun, General Director of Shinhan Life Vietnam. — Photo courtesy of the company |

"We are focused on building and developing our product portfolio, distribution channels, and operating model. These are the steps we will take to create differentiation in the Vietnamese market," shared Mr. Bae Seung Jun, General Director of Shinhan Life Vietnam, in an interview with Việt Nam News.

Given the challenging economic environment and the insurance market's specific challenges, many insurance companies had to adjust their strategies. How about Shinhan Life?

Since Shinhan Life entered the Vietnamese insurance market later than other companies, we need to create something unique as a competitive advantage. The three key sections of differentiation will be our products, distribution channels, and operational model.

I understand that the current situation in Việt Nam, like many other economies, is facing difficulties, especially in the insurance sector. Therefore, at Shinhan Life, we are closely monitoring the market and consulting with our parent company in South Korea to gain the most accurate direction. South Korea's insurance market has also experienced similar fluctuations in the past. South Korean customers are meticulous, detail-oriented, and value customer rights. We can leverage the lessons learned from our parent company to enhance service quality and design products that meet the increasing standards of Vietnamese customers. Simultaneously, we have plans to focus on training, and improving the expertise and ethics of our advisory team to serve customers better.

|

| Shinhan Life Vietnam has three key sections of differentiation in the Vietnamese insurance market. — Photo courtesy of the company |

Shinhan Life's business development strategy still involves distributing insurance through banks, financial companies, and digital platforms, is it correct, sir? Do you have plans to expand into other distribution channels in the future?

Shinhan Life’s bancassurance channel focuses on customers with good incomes who are concerned about asset management and investment products. For younger customers or those with protection needs, we will distribute insurance products with reasonable coverage and premiums through telemarketing and through partner distributors.

Furthermore, Shinhan Life Vietnam is preparing to launch the professional Financial Consultant channel (FC) next year with a focus on the quality of the personal insurance agency. We will also leverage the strengths of other member companies within the Shinhan Financial Group to collaborate and enhance differentiation from other insurance companies.

What are your thoughts on the importance of the agency channel in emerging markets like Việt Nam, where insurance companies can proactively ensure both quality and quantity?

Due to the complexity of insurance products, in-person consultant agents are essential for helping customers understand their own needs and the features of the products. Therefore, I believe that the agency channel remains important in the present and future.

Regarding the role of insurance agents (or financial advisors), if in the past, they only focused on product advice, the market trend going forward will require them to become more professional. Financial advisors should not only advise on products but also guide customers on their personal and family financial situations to provide the most suitable financial solutions. Therefore, financial advisors will need to invest in training and time for their jobs to become professional financial experts and keep up with market trends and the times.

Our professional agency channel is still in the preparation stage and will officially launch next year. We will not focus on quantity but rather on quality, recruiting highly experienced personnel for a solid foundation.

|

| Shinhan Life is trying to enhance the quality of life for Vietnamese customers. — Photo courtesy of the company |

Regarding the product strategy, the market has witnessed a sharp decline in revenue from previously popular insurance products, especially unit-linked insurance products. How does this affect Shinhan Life's product development strategy?

The market is shifting towards a focus on customer rights, so in the future, companies need to develop a product portfolio that better suits customers' actual needs. Besides investment-linked insurance products, I believe that protection-focused products, such as health insurance, will also gain more attention from customers.

Currently, only about 11 per cent of Việt Nam's population is insured, so more people are expected to buy life insurance, creating opportunities for insurance companies. Joining the market later is also an advantage for Shinhan Life because we can develop step by step, adapting to market dynamics and the market's development patterns.

I would also like to share that Shinhan Life aims to become a leading insurance company in protection-focused insurance products. We believe this is a niche market that other companies have not focused on much, while we anticipate a strong increase in demand for insurance, particularly health insurance, in the near future. Additionally, Shinhan Life will continue to develop other products, such as investment-linked products, to diversify our product portfolio.

|

| “Shinhan Life aims to become a leading insurance company in protection-focused insurance products,” said the General Director of Shinhan Life Vietnam. — Photo courtesy of the company |

The recently amended insurance business law has introduced several new, tighter regulations for controlling insurance product distribution through bank channels. How do these adjustments affect the market, and what are your forecasts for the market in the near future?

It is true that many legal regulations regarding the insurance business are becoming stricter, especially in the distribution of insurance products through bancassurance channels. However, I see these changes as positive because they not only focus on improving the quality of insurance companies' operations but also require insurance companies to prioritize customer rights.

As insurance companies are intensifying efforts to enhance the quality of their sales team, sales processes, and customer services, I believe that the insurance industry, in general, will regain customer trust. This, in turn, will help the life insurance market recover and grow in the near future. — VNS

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Talking Shop

Việt Nam and Singapore will celebrate 50 years of diplomatic relations this year, while Singaporean FDI remains sky-high. We interview the CEO of the Singapore Business Federation to learn what makes the country so attractive to Singaporean businesses.

Talking Shop

Talking Shop