HCM CITY — HSBC Global Research's latest report, from Tuesday, has stressed the country's potential upgrade this year to emerging market status.

The report 'Việt Nam at a glance - Let’s talk capital' emphasises the country's expanding capital mobilisation channels and provides insights into trade, imports, exports and tariffs.

|

| Việt Nam’s economic growth has been financed primarily by an expansion in bank credit. — Photo courtesy of the bank |

Việt Nam was the best stock market performer in Southeast Asia in 2024.

However, recent quarters have also seen some pullback in portfolio investment flows from foreign investor. Albeit mostly driven by macro developments, this nevertheless poses the question, are there roadblocks inhibiting foreign interest and participation in Việt Nam’s stock market? And indeed, structural challenges persist, says the report.

These include transaction and infrastructure-related hurdles, relatively less corporate transparency and disclosures.

But changes are underway. Effective November 2024, Việt Nam has scrapped the pre-funding requirement for stock market transactions, clearing a significant criterion to upgrade its designation from a frontier market to an emerging market, potentially later this year. The country has been on the watchlist since 2018. If implemented, FTSE Russell, a major index provider, estimates that an upgrade in designation could bring US$6billion or over one per cent of GDP in foreign investment inflows into the country.

|

| A SeaBank employee checks money for a client. — Photo courtesy of Vietnamplus |

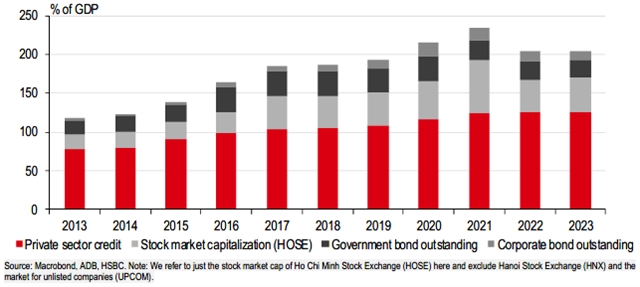

Such focus is particularly significant for Việt Nam, which has lagged ASEAN peers in terms of stock market development. In contrast, bank lending has grown substantially relative to the size of its economy, indicating that credit primarily supported the high growth trend observed over the years.

However, a large dependency on credit can lead to amplifying economic adjustments in an adverse manner, such as when borrowing costs rose in late 2022. When the economy experienced acute inflation shortly after the pandemic and the State Bank of Việt Nam (SBV) responded accordingly by tightening monetary policy, credit growth slowed sharply as pressures flowed across many areas in the domestic sector, particularly in banking and real estate, which is included under other services.

In this context, developments to improve capital markets should not only be seen as catching up to market peers but also in terms of diversifying and expanding capital mobilisation channels to build financial resilience.

Despite the stock market being larger in size relative to its bond market, actual capital raised in the equity market only amounted to ten per cent of funds raised in the corporate bond market through 2019-23. The dominant presence of the banking sector is also reflected in these markets, of which the banking sector traditionally and continues to encompass the majority of corporate bond issuances. Other sectors, such as manufacturing and retail, evidently face greater challenges in accessing sources of funding other than bank credit, potentially limiting an efficient allocation of capital and constraining activity.

|

| Stock tradinh figures seen on a monitor screen in a brokerage house in Hà Nội. — Photo Vietnamplus.vn |

The Government has been taking steps to address various challenges and risks surrounding capital markets. Following the challenging market environment for corporate bonds in late 2022, the authorities have introduced more safeguards to allay investor concerns, such as allowing only professional investors to participate in the trading of corporate bonds via private placement.

Meanwhile, structural reforms to improve transparency and information disclosure to accommodate a global investor base are also underway. In comparison to other ASEAN peers that have already adopted International Financial Reporting Standards (IFRS), not all corporations in Việt Nam have shifted from Việt Nam Accounting Standards (VAS) and adopted IFRS yet, leading to valuation differences. Encouragingly, 2025 is a key year in the transition plan set forth by the government, as IFRS adoption shifts from being voluntary to compulsory for public companies from this year onward.

Introducing more transparency has also been the case in other areas of the economy, such as the real estate market. Regulatory changes in the 2024 Land Law, 2023 Housing Law, and 2023 Real Estate Business Law have supported newly registered FDI to flow into the sector, registering $4 billion in 2024, up from $1billion in 2023. Notable changes, such as land prices better reflecting market values, easing land-related rights for overseas Vietnamese, and more stringent information disclosure by real estate businesses, will continue to support a recovery in sentiment.

Beyond increasing foreign participation in capital markets, expanding and diversifying the domestic investor base will be key in helping to sustainably achieve the official targets of a stock market capitalisation of 120 per cent and corporate bonds outstanding of 25 percent of GDP, respectively, by 2030. Indeed, the presence of institutional investors in both spaces has notable room to grow. — VNS

Politics & Law

Politics & Law