Economy

Economy

Tân Sơn Nhất temporarily suspends flights after UAV sightings

1.

The introduction of a credit package to finance high-tech agriculture has been lower than expected due to many barriers.

|

| A vegetable garden in Đà Lạt City in the Central Highlands province of Lâm Đồng using automatic watering system. Agriculture production applying advanced technology has received a lot of support from the Government, including a stimulus credit package. — VNA/VNS Photo Nguyễn Dũng |

HÀ NỘI — The introduction of a credit package to finance high-tech agriculture has been lower than expected due to many barriers.

In March this year, Prime Minister Nguyễn Xuân Phúc told the State Bank to instruct commercial banks to set aside at least VNĐ100 trillion (US$4.4 billion) from mobilised capital to lend to high-tech agricultural activities.

The credit package carries interest rates 0.5-1.5 percentage points lower than current commercial levels.

According to the State Bank of Việt Nam (SBV), commercial banks have so far committed to provide total VNĐ120 trillion under this package. Total outstanding loans in the field of hi-tech and clean agriculture has so far reached nearly VNĐ32.3 trillion, accounting for nearly 27 per cent of the package.

Nguyễn Quang Huy, chairman of the Huy Thuận Seafood Investment Ltd Co, said capital was one of pressing needs of agricultural producers. The difficulty in accessing loans is a factor that hinders local ability to compete with foreign bussinesses.

“The credit package brings hope that more and more enterprises will be willing to invest in high-tech agriculture development,” Huy said.

However, Lại Xuân Môn, chairman of the Vietnam Farmer’s Association, said commercial banks actually hesitated to disburse the capital.

Nguyễn Cảnh Hậu, head of Corporate Banking Division of the Việt Nam Bank for Agriculture and Rural Development (Agribank)’s Hòa Bình branch, said that the bank was confused when trying to provide credits to enterprises as there were no specific criteria to determine what high-tech farming is.

Sharing the same opinion, representatives of Việt Nam Joint Stock Commercial Bank for Industry and Trade (VietinBank) also said that without the criteria, it would be hard to tell the difference between high-tech agriculture, clean agriculture and organic agriculture.

High-tech agriculture often needed large amounts of capital with long-term disbursement, but this was very risky for banking business, Môn said.

Collateral issue

In fact, collateral is also one of the challenges for businesses when accessing this capital source. According to banks, collateral obtained from the use of loans is currently inadequate.

Besides, owners of some facilities built on land they lease for agricultural production such as green houses or net houses are not granted certificates of ownership for the property, thus they could not be used as collateral for borrowings.

Agribank chairman Trịnh Ngọc Khánh quoted by baochinhphu.vn as saying “When we have a bumper crop, these facilities are very valuable, but when the agricultural production is hit by natural disasters, a VNĐ500 billion factory could be worthless.”

In reality, many high-tech farming firms have to lease land from rural households and they don’t have the ownership right to the land plots, thus could not mortgage them for banking loans.

Dương Thị Quỳnh Liên, director of Vân Hội Safe Vegetable Cooperative in the northern province of Vĩnh Phúc, said that to borrow capital from banks, "we have to have some things used as collateral, but the co-operative has nothing". Her co-operative’s headquarter is leased and production land is owned by farmers and co-operative farmers.

“We mostly obtain trust loans,” Liên said.

However, the unsecured loans were only feasible based on transparent, reliable and trustworthy information, the Vietinbank representive said, adding that otherwise it was very risky for banks.

Nguyễn Đức Hưởng, chairman of LienVietPostBank, said that other challenging problems were related to farm produce consumption.

Hưởng said “When we have bumper crops, prices drop” but “when we have poor harvests, prices hike”. This is a vicious circle that has not resolved thoroughly. Therefore, many banks are not very keen on lending for agricultural production, he added.

Preferential credit policy

In order to remove difficulties for enterprises, and at the same time open credit capital for hi-tech agriculture, Nguyễn Hồng Phong, general director of Tiến Nông Agro-Industry Joint Stock Company in the central province of Thanh Hóa, said it was necessary to classify hi-tech agriculture projects according to different priority levels and preferences suitable to each type of enterprise or households.

According to him, besides large enterprises that have the advantage of accessing capital, small and medium enterprises (SMEs), especially farmers, find it difficult to meet all lending criteria. Meanwhile, SMEs are more interested in investing in this sector, contributing significantly to its development.

As for the output-related issues, Hưởng from LienVietPostBank suggested that the Government should have incentive policies for businesses to collect and sell farm products.

Forms of cooperation among farmers, especially between farmers with enterprises, aim to invest in production expansion, create stable production, improve quality of agricultural products, and build a prestigious brand name.

According to Hưởng, businesses need to develop production chains from production to processing and consumption of products to increase added value of high-tech agricultural products and improve competitiveness in the market. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

The southern province of Bình Dương will focus on the attraction of investment in hi-tech industries that are less labour intensive and more environmentally friendly.

Economy

Economy

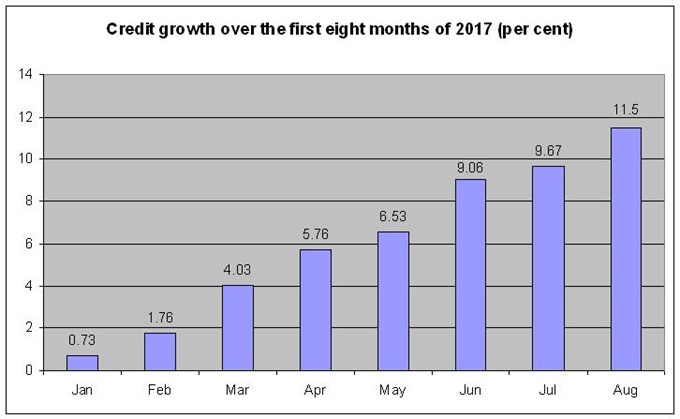

Credit growth rate in the first eight months of 2017 has been estimated at 11.5 per cent compared to the end of 2016, the National Financial Supervisory Commission (NFSC) reported.

Economy

Economy

Hà Nội’s economy has expanded since the beginning of this year with steady growth recorded in all key sectors of industry, trade, tourism and services and agriculture, reported the municipal People’s Committee.

Economy

Economy

It’s expected to be a strong September on the local stock market, as investors are maintaining confidence after positive economic data in August and a period of prolonged net buying by foreign traders.

Economy

Economy

A new full-moon season starts in one month and confectioneries nationwide are ready with many kinds of mooncakes with new flavours.

Economy

Economy

Foreign online travel agencies have been dominating the online tourism market in Việt Nam.

Economy

Economy

The Ministry of Finance has held a meeting to introduce changes in the list of Việt Nam’s export and import goods as per Circular No 65/2017 / TT-BTC.

Economy

Economy

The State Bank of Việt Nam (SBV) has issued a draft amendment updating a new circular regulating capital ratios for the operation of credit institutions and foreign bank branches.

Economy

Economy

The Hà Nội Stock Exchange (HNX) will assess and honour the top 30 listed companies for best corporate governance in November during its annual convention for listed businesses.

.jpg)