Economy

Economy

Digital transformation gives Đồng Tháp tourism a boost

1.

Poised for prodigious purchasing power in near future, Việt Nam is barely tapping into its market potential for consumer loans, with which come the needs for national spending boost and further economic growth.

|

| Customer borrows loan at a branch of VPBank. — VNA/VNS Photo |

HÀ NỘI — Consumer lending has the potential for explosive growth in Việt Nam, but this can only happen with significant improvements in consumer satisfaction with credit institutions and loan conditions, experts say.

They say that tapping this growth potential will boost national spending and economic growth.

“Within the decade, market demand for unsecured loans has grown to adapt to the current financial scene in Việt Nam, with an increasing amount of retail lenders and personal borrowers,” Hoàng Văn Hải, Director of the School of Business Administration (SBA), Vietnam National University of Economics and Business, said at a conference last week.

He said the growth can be attributed to favourable legal and socio-economic conditions that have fostered changes in income and spending habits.

At present, consumer loans in Việt Nam range in value from VNĐ1 million to VNĐ60 million ($44.6 to $2680). The application process and repayment schedule are fairly simple, and the rate of interest is reasonable at between1.49 per cent to 1.6 per cent per month, with the occasional zero per cent for smaller loans.

In 2016, consumer credit was mostly used for purchasing household goods and travel expenses, with a focus on mobile devices, vehicles and personal computers under $2000. Sometimes, depending on the borrower’s credit history, capital is given directly (instead of paying purchase invoices).

Vietnamese consumers are reaching a spending over earnings ratio of 67 per cent, and this is set to rise further as the economy picks up.

Hải said that Việt Nam will soon reach a purchasing market worth about $15 billion per year, with 30 million people in the 20 to 59 age bracket.

This means more and more people in the middle income group are demanding capital to fund their immediate spending, without the hassle going through bank loans for smaller purchases.

Underdeveloped sector

However, the central bank sees current retail lending as underdeveloped, given the modest number of credit institutions giving out consumer loans as also the overall demand for such loans.

The central bank estimates that consumer loans account for just five to ten per cent of total lending in the country, as opposed to the average 40 to 50 per cent in developed nations.

Cấn Văn Lực, a senior advisor to the Chairman of the Joint Stock Commercial Bank for Investment and Development of Vietnam (BIDV), said at an online conference in March that Vietnamese credit institutions granting consumer loans have a mere US$1.78 billion in capital, about 0.7 per cent of the credit sector’s total.

This is due to the fact that these institutions are not allowed to take deposits like commercial banks, having to rely instead on bonds.

The lack of capital, coupled with the reluctance among a majority of consumers to borrow, has lead to interest rates higher than the commercial banks’ average of 0.9 to 1.2 per cent per month, said Lực.

However, consumer lending carries rich potential, especially among the population segment that does not qualify for bank loans. This segment can access this capital instead of being beholden to black market loans controlled by loan sharks.

While the central bank is positive about growth in this credit segment, there are still regulatory issues that need to be resolved.

In 2016, the SBV and the Ministry of Industry and Trade, received a large number of complaints from borrowers.

The Vietnam Competition Authority (VCA) released a report last year in which they detailed several major problems faced by consumers buying common household and electronic items.

A chief complaint from borrowers was that cumulative calculation of interest rates made the loan repayment untenable in just three to six months. They also said that the credit institutions did not show “decent conduct” while trying to recover loans.

The VCA advised consumers to have a clear understanding of the loan contracts before signing and reevaluate their own disposable income before taking out a loan, no matter how small.

Meanwhile, the SBV has simplified procedures and increased transparency for consumer loans through Circulars 39 and 43 issued in 2016 and 2017 respectively.

At present, the SBV considers a loan to be a consumer loan if it is made in Vietnamese Đồng, the borrower is an individual, not an institution, the purpose of the loan is to meet personal spending needs, and the total amount borrowed does not exceed VNĐ100 million ($4468). — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

.jpg) Economy

Economy

Economy

Economy

April had the highest number of newly-established enterprises in the past 12 months, according to the Ministry of Planning and Investment’s National Enterprise Information and Registration System.

Economy

Economy

The national index of industrial production (IIP) in the first four months of this year increased 5.1 per cent year-on-year, the General Statistics Office (GSO) reported.

Economy

Economy

The Kiên Giang Province People’s Committee has approved a plan to make Phú Quốc a smart city by 2020.

Economy

Economy

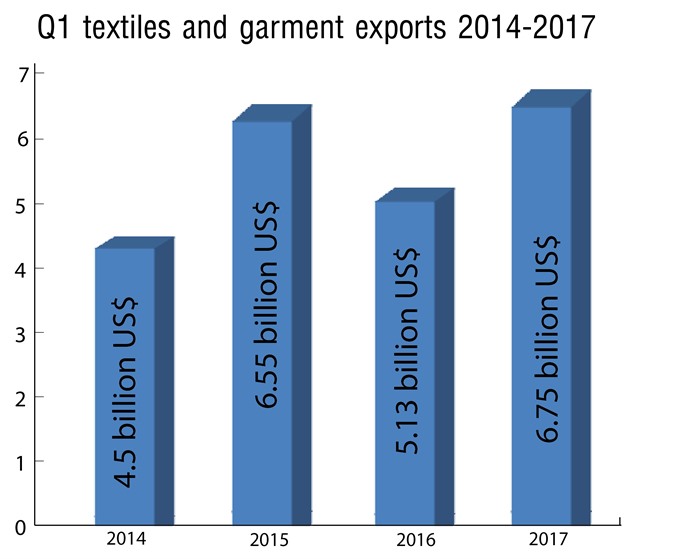

The textile and garment sector enters the second quarter (Q2) of this year with promising signs from new import markets, said General Director of the Việt Nam Textile and Garment Group (Vinatex) Lê Tiến Trường.

Economy

Economy

Economy

Economy

Shares advanced during the first session on Wednesday after the National Reunification and International Labour holidays as investors remained positive about the market outlook.

Economy

Economy

The Asian Development Bank (ADB) this year plans to provide loans worth US$4.2 billion, doubling last year’s figure, to support developing countries in the Asia-Pacific region in addressing water challenges.

Economy

Economy

The Đại Nam Joint Stock Company opened an international standard racecourse with investment of more than VNĐ2 trillion (US$87.9 million) in the southern province of Bình Dương on Tuesday.

Economy

Economy

Total export turnover of the northern province of Quảng Ninh hit US$461.3 million in the first four months of 2017, making up 28 per cent of the yearly plan.