Economy

Economy

New policy may have adverse impacts on bancassurance

The regulation under the amended Law on Credit Institutions was recently passed by the National Assembly and will take effect from July this year.

|

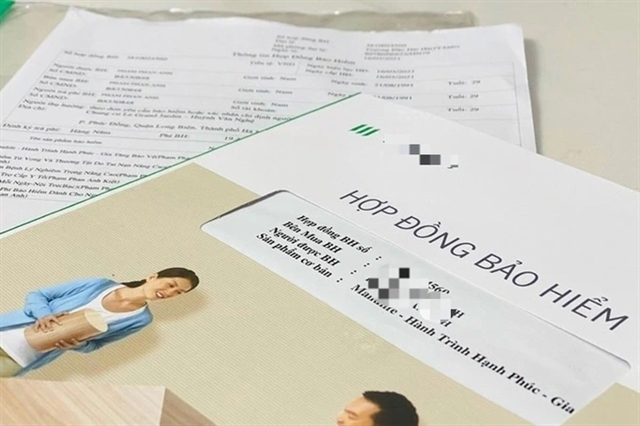

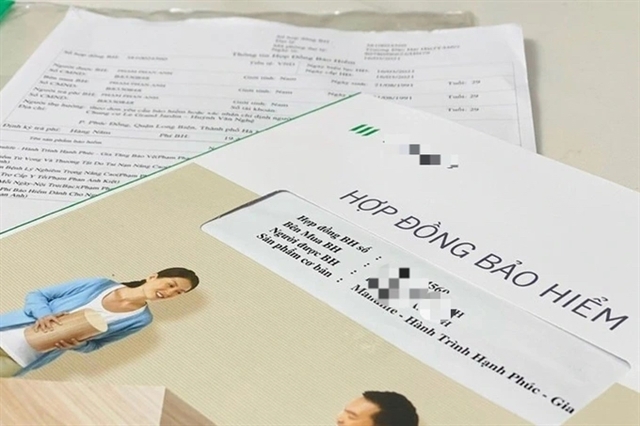

| A customer during a policy consultation. Some banks have had to temporarily suspend the sale of insurance products, causing their revenue to decline sharply since the law took effect. Photo courtesy of Baoviet Life Corp |

HÀ NỘI — Insurance companies are awaiting further details on regulations that will guide the implementation of a new policy on banning the sale of insurance products through banks (bancassurance) to help them comply with the law.

Clause 5 of Article 15 of the Law on Credit Institutions, which took effect on July 1 this year, prohibits banks from ‘linking’ the sale of non-mandatory insurance products with the provision of banking products or services in any form.

However, insurance companies state their biggest current problem is the ongoing confusion about applying and understanding this specific clause, which is causing a loss of revenue.

According to insurance companies, not only banks and insurance companies but also local management agencies lack clarity and hold different intepretations of Clause 5 of Article 15.

Many of their questions about the provision remain unanswered, such as what qualifies as a ‘non-mandatory insurance product?’, or what constitutes ‘linking’ the sale of non-mandatory insurance products with the provision of products and services in ‘all forms.’

For example, regarding the concept of ‘linking’, some understand the regulation banks cannot force borrowers to buy insurance products, while others think it means banks are not allowed to give any advice or offer insurance products when processing loan applications for customers.

So far, there has been no unified and specific guidance about Clause 5 of Article 15 from the authorities.

General Director of Agribank Insurance Company Nguyễn Hồng Phong said that previously, 80 per cent of the insurer’s revenue came from insurance sales through Agribank. However, since July 1 this year, when the Law on Credit Institutions took effect, many Agribank branches had to stop selling insurance products, resulting in revenue losses for both insurance companies and banks.

According to Phong, on October 11, the State Bank of Vietnam year sent a document to the Vietnam Banks Association regarding the implementation of Clause 5 of Article 15. Howver, Phong believes that the SBV should issue a circular on the matter to ensure unified understanding and implementation of the regulation.

Deputy General Director of insurance company BIC Đoàn Thị Thu Huyền also said Clause 5 of Article 15 imposes strict regulations, but the lack of a guiding decree or circular leads to different understandings.

In addition, the law also does not clearly distinguish between life and non-life insurance. Therefore, Huyền proposed an official circular be issued to guide this issue. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Bancassurance activities will have to strictly comply with the provisions of the Law on Insurance Business, according to the State Bank of Vietnam (SBV).

Economy

Economy

Local credit institutions are enjoying a rise in bancassurance activities with more exclusive deals coming, according to industry insiders.

Economy

Economy

Economy

Economy

Banks are pushing the sale of life insurance products (bancassurance) in the context of low credit growth since the beginning of this year due to the impacts of the COVID-19 pandemic.

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

.jpg) Economy

Economy

Economy

Economy

Economy

Economy

.jpg) Economy

Economy