Economy

Economy

HCM City police bust laughing gas ring, eight detailed

1.

Moody's has assigned Vietcombank and Maritime Bank local currency deposit ratings of B1/NP for Vietcombank and B3/NP for Maritime Bank.

|

| A Vietcombank transaction office in Hà Nội. Vietcombank’s ratings outlook on the issue and deposit ratings is stable.- VNA/VNS Photo |

HÀ NỘI – Moody’s on Thursday assigned first-time ratings this year to Vietcombank and Maritime Bank.

According to reports released on its website, Moody’s assigned local currency deposit ratings of B1/NP; foreign currency deposit ratings of B2/NP; a baseline credit assessment (BCA) of B2; and an adjusted BCA of B2 to the Bank for Foreign Trade of Việt Nam (Vietcombank).

Vietcombank’s ratings outlook on the issuer and deposit ratings is stable.

Moody’s has also assigned counterparty risk assessments (CR Assessment) of B1(cr)/NP(cr) to the bank.

Vietcombank’s B1 local currency deposit rating has been raised by one notch from its B2 BCA.

“We do not incorporate any affiliate support assumptions from Mizuho Bank, Ltd (Mizuho) [A1 stable, Baa1] into Vietcombank’s supported ratings, because of its relatively small ownership stake of 15 per cent,” Moody’s said.

According to Moody’s, the B1 local currency deposit rating assigned to Vietcombank reflects the combination of the bank’s B2 baseline credit assessment (BCA), and a one-notch rise for expected support from the government of Việt Nam (B1 stable) in case of stress. Vietcombank’s foreign currency deposit rating is positioned at B2, in line with Việt Nam’s foreign currency deposit ceiling.

Headquartered in Hà Nội, Vietcombank reported total assets worth VNĐ662 trillion (US$29.3 billion) as of March 31, 2016.

On the same day, Moody’s also assigned local and foreign currency issuer ratings of B3/NP; local and foreign currency deposit ratings of B3/NP; a standalone baseline credit assessment (BCA) of Caa1; and an adjusted BCA of Caa1 to Việt Nam Maritime Commercial Joint Stock Bank (MSB).

MBS’s ratings outlook on the issue and deposit ratings to Maritime Bank is positive.

According to Moody’s, MSB’s B3 long-term ratings reflect the bank’s baseline credit assessment (BCA) of Caa1 and a one-notch jump due to Moody’s expectation of moderate support from the government of Việt Nam (B1 stable), in case of stress.

According to Moody’s, MSB’s profitability is weak mainly because of its high loan loss provisions. The bank channelled 77 per cent of its pre-provision income into reserves in 2015, down from 82 per cent in 2014.

Moody’s expects MSB’s provisioning expenses to remain high in 2016 and 2017, as the bank gradually works out its problem exposures.

MSB’s liquidity position is robust, with liquid assets accounting for about 52 per cent of the total assets. Customers constituted 69 per cent of the total liabilities at the end of 2015, of which the majority was derived from individuals.

“While the BCA of Caa1 indicates that the bank is operating under regulatory forbearance, the positive outlook on the supported ratings reflects the bank’s committed and ongoing efforts to resolve its legacy of problem assets, which should lead to improved asset quality and profitability metrics. Given the large size of these legacy accounts and positive expectations around recovery, this could lead to meaningful improvements in asset quality within the year. If successful, the material recovery of impaired assets could significantly improve the bank’s solvency profile,” Moody’s said.

The moderate systemic support assumption for MSB is based on the bank’s modest 1.3 per cent share of system deposits at the end of 2015, as well as a strong history of regulatory forbearance in Việt Nam. These resulted in a one-notch rise in its rating to reach B3, above the bank’s Caa1 BCA, Moody’s said. - VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

PetroVietnam Power Corporation (PV Power) plans to sell its entire 2.88 million shares or 7.85 percent stake in affiliate EVN International JSC in Hà Nội on August 1.

Economy

Economy

Despite the Government’s willingness to enter into free trade agreements, Vietnamese companies are not taking advantage of such pacts to increase exports and are even losing out on their home turf to foreign rivals.

Economy

Economy

The State Bank of Việt Nam will keep track of gold price fluctuation and intervene if necessary, said Nguyễn Ngọc Cảnh, director of the bank’s Foreign Exchange Management Department.

Economy

Economy

The Hà Nội Stock Exchange (HNX) has mobilised VNĐ212 trillion (US$9.46 billion) in government bonds for the State budget in the first half of this year, said Nguyễn Thành Long, the exchange chairman.

Economy

Economy

The domestic railway industry should reform to increase its competitive ability and revenue in the second half of this year, an official of the Ministry of Transport has said.

Economy

Economy

While the imposition of additional tariffs on imported steel products as a temporary safeguard against cheap imports since March was meant to protect the local steel industry, consumers and firms that use steel for their production are worried about steel price hikes in the local market.

Economy

Economy

State price management agencies will face many challenges in the second half of the year if they are to meet the National Assembly’s (NA) target of keeping inflation under 5 per cent, experts said at a conference held yesterday.

Economy

Economy

Vietnamese shares advanced yesterday as investors were upbeat on an uncertain US interest rate increase and higher oil prices helped energy firms rebound.

Economy

Economy

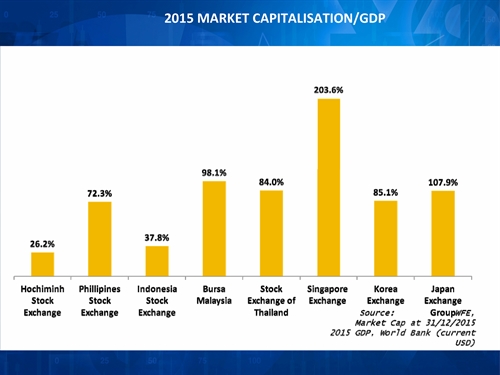

With the combined market capitalisation of all listed companies accounting for less than 30 per cent of the country’s GDP, the Vietnamese securities market has plenty of room to grow, Trần Anh Đào, deputy director of the HCM City Stock Exchange (HOSE), said yesterday.