Economy

Economy

No additional Vietnamese casualties reported in Japan quake: Consulate General

1.

|

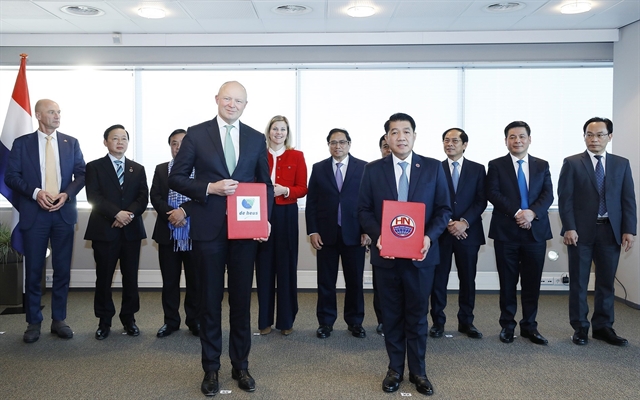

| A transaction office of Vietcombank in Hà Nội. Vietcombank topped the list with the highest loan-loss reserve ratio of 402 per cent. VNA/VNS Photo |

HÀ NỘI — Amid rising non-performing loans (NPLs), many banks have strongly increased their loan-loss reserve (LLR) funds to readily face uncertainties in the future.

According to experts, the move is a positive signal reflecting the preparation of banks for unpredictable fluctuations.

The impact of the COVID-19 pandemic, coupled with a tight monetary policy, spelt trouble for Việt Nam’s economy, especially deteriorating bank asset quality. Banks reported a strong surge in NPLs in Q3 2022, resulting from the expiry of Circular No. 14/2021/TT-NHNN, which allowed banks to reschedule the loan payment time and maintain the same debt group for COVID-19-affected borrowers, at the end of June this year.

Financial statements of 27 banks showed the banks’ on-balance sheet NPLs in the year through September amounted to nearly VNĐ129.8 trillion, up 28.4 per cent against the figure earlier this year. Of the total, potentially irrecoverable debts skyrocketed by 62.5 per cent to VNĐ72.4 trillion, accounting for 55.8 per cent of the total NPLs, up 11.8 per cent over January.

To deal with the rising bad debts, 14 out of 27 banks strongly increased their LLR ratio in the first nine months of this year, Q3 2022 financial statements of banks showed.

Among the banks, Vietcombank topped the list with the highest LLR ratio of up to 402 per cent. To put it another way, Vietcombank has set aside VNĐ4.02 for every đồng in bad debt.

VietinBank also raised its LLR ratio to 250 per cent by late September, up 70 per cent compared to late 2021.

BIDV, Military Bank, Bắc Á Bank, Techcombank and Sacombank also hiked their ratio to 214 per cent, 208 per cent, 190 per cent, 165 per cent and 154 per cent, respectively.

Trần Thị Khánh Hiền, head of VNDirect Securities Company’s analysis division, said though banks’ bad debts increased in the third quarter of 2022, their provisions for defaulted loans were still well guaranteed and higher than that at the end of 2020 and 2021. It was a positive signal as banks have readily prepared for increasing bad debt risks in the future.

According to banking expert Dr. Nguyễn Trí Hiếu, the loan loss provision coverage ratio is an indicator of how protected a bank is against future losses. A higher ratio means the bank can withstand future losses better, including unexpected losses beyond the loan loss provision.

“High LLR ratio shows the bank's willingness to use the provisions to write off defaulted loans. This is a solid buffer for possible shocks in the future. Profits of banks, which have increased their LLR ratio to more than 100 per cent, will not be affected even if all their NPLs become defaulted,” Hiếu told Việt Nam News.

Besides, he said, part of this provision could be reversed when the debt is recovered, and converted into profit.

Việt Dragon Securities Company (VDSC) also believes profits of many banks, which have already made adequate provisions for restructured debts according to Circular 14, will not be under pressure from the expiry of the circular. Vice versa, banks, which have not set aside enough for provisions, will face the possibility of rising credit costs.

Though a bank leader, who declined to be named, admitted a recent increase in profits created favourable conditions for many banks to build a solid provision buffer, it would not be easy for the domestic banking industry due to global uncertainties.

The bank leader was cautious in predicting that uncertainties in the near future might cause bank profit growth to be no longer as strong as before, which would cause bad debt risks to rise and provision buffer to decline.

In a recent report, Agribank Securities Company (Agriseco)’s analysts also forecast banking profits in 2022 and 2023 will find it difficult to maintain the same high growth as the previous two years as there is not much room for credit growth while profit margins are under pressure due to rising input costs.

VNDirect’s Hiền admitted the pressure on interest rates might last until the first half of 2023, depending on the interest rate management moves of the US Federal Reserve (Fed).

In addition, she said, higher lending interest rate expenses were reducing the profitability of enterprises and increasing debt pressure.

On the other hand, limited bank credit room and tightly controlled corporate bond issuance were also making it hard for many firms to arrange capital for their production and business, which could adversely affect the asset quality of banks from 2023 onwards, Hiền noted.

However, Hiền is optimistic that banks with healthy asset quality will have an advantage in facing the risks, saying bank profit is forecast to grow steadily if the bank is allocated high credit growth cap while having a high demand deposit ratio, a low loan-to-deposit ratio, and a low ratio of short-term funds used for medium and long-term loans.

Besides focusing on increasing provision buffer, many banks are also rushing to sell collateral to accelerate the handling of defaulted debts. Some of them even offered a big discount for the assets under the current unfavourable economic environment, with 16 banks having sold debts and collateral worth some VNĐ32 trillion via the debt exchange of the Việt Nam Asset Management Company. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy