Opinion

Opinion

ASEAN educators gather in HCM City to map out future of AI-driven higher education

1.

|

| A production line at a Vietnamese brewery. Experts propose a balanced approach and long-term roadmap for increasing the special consumption tax on alcohol and beer to avoid policy shocks and support the industry. Photo Sabeco |

The Ministry of Finance has just announced a draft amendment to the Special Consumption Tax Law. This draft proposes imposing an 80 per cent special consumption tax on spirits with an alcohol content of 20 degrees or more and on beer by 2026, with gradual increases each year, reaching 100 per cent by 2030. For spirits with an alcohol content below 20 degrees, the Ministry proposes a 50 per cent tax from 2026, rising to a maximum of 70 per cent by 2030.

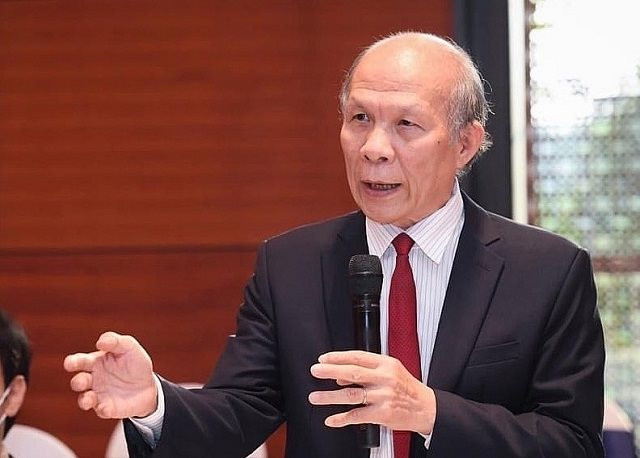

Nguyễn Ngọc Tú, a tax expert, former Editor-in-Chief of the Tax Journal and currently a lecturer at the Hanoi University of Business, talks to Sài gòn giải phóng (Liberated Saigon) about the matter.

The draft amendment to the Special Consumption Tax Law recently announced by the Ministry of Finance includes provisions for increasing the Special Consumption Tax on alcohol, beer and sugary soft drinks, which has attracted public attention. What are your thoughts on this draft?

The main objective of this tax is to regulate consumer behaviour and manage goods and services that are not essential and are not encouraged for use due to environmental, public health and social welfare reasons.

Currently, the Special Consumption Tax on alcohol, beer and alcoholic beverages is already between 60 and 65 per cent. Looking at these figures compared to the tax rates, Việt Nam still has room to continue increasing the Special Consumption Tax. However, beyond international practices and theoretical bases, each country sets its Special Consumption Tax based on its own management conditions, socio-economic conditions, income levels, and specific consumption habits and customs. The goal is to avoid a policy 'shock'.

For alcohol and beer in Việt Nam, besides tax policies, there have also been a series of other policies affecting these products, such as the Law on Road Traffic Safety and Order, the Law on Prevention and Control of Alcohol, Beer, and Tobacco Harms and regulations on blood alcohol content for drivers. Consumer behaviour towards alcohol and beer has gradually decreased, indicating that we have achieved the intended purpose.

In a recent petition to the government, the Việt Nam Beer, Alcohol, and Beverage Association (VBA) suggested that authorities consider extending the roadmap for increasing the Special Consumption Tax. Do you think the proposed roadmap in the draft is reasonable?

In my opinion, the issue that needs attention is the impact on production and business enterprises. What effects will they face and how will these impacts affect state tax revenue?

I believe the Special Consumption Tax policy should consider a longer-term roadmap than what the Ministry of Finance's draft proposes and should take into account various impacts. If there is a need to increase the tax, there should be a long-term plan, with each step spanning at least 10 years. For instance, when currently building the Special Consumption Tax, the minimum roadmap for each step should extend to 2035 or 2045. This is to avoid 'jerky' policy changes that make it difficult for businesses to adapt. Additionally, sometimes in Việt Nam, policy amendments are made without sufficient consideration, resulting in policies that, when implemented, do not achieve the desired effectiveness.

When a tax policy is applied, it impacts not only consumers but also businesses. Each business has its own policies and development plans, and some have recently invested in production lines and machinery with life cycles of 5-10 years. When tax policies change, businesses may not be able to adapt quickly and will certainly incur losses. Therefore, tax policies need to be planned with an appropriate roadmap.

Looking back at the 12 times the Special Consumption Tax on alcohol, beer, and alcoholic beverages has been reformed since 1990, we can see this tax's regulatory nature, characteristics, and complexity. There have been times of intense debate. The reason is that the benefits of the three main stakeholders - the state (management agencies), businesses (producers, distributors) and the public (consumers) - were not harmonised.

When the drafting agency sets tax calculation methods, tax rates and policies, they must ensure consistency to provide stability for businesses in their investment and production operations. Changes in policies undoubtedly affect the business community, so it is essential to avoid excessive risks when adjusting policies.

As you mentioned, the important aspect of a policy (including tax policy) is to consider and carefully review its feasibility and effectiveness after enactment. Some policies may seem reasonable in theory but fail to achieve the desired results in practice. Can you elaborate?

Policy formulation must aim for harmony. Although Việt Nam's economy has grown significantly, it remains a developing economy with relatively low per capita income despite improvements. Businesses are still small-scale and have low competitiveness.

In summary, although domestic businesses have made progress, their competitive capacity is still limited. Therefore, any tax policy must be carefully considered to avoid adding undue burdens on both the public and businesses.

Tax policy formulation must meticulously consider the impacts and feasibility. Increasing the Special Consumption Tax requires synchronised tax administration. For example, if the Special Consumption Tax on alcohol and beer is raised to 100 per cent, how will tax administration for these products be managed, given that traditional alcohol production remains unregulated?

This scenario could lead to tax inequity. Moreover, controlling alcohol and beer smuggling becomes crucial. Higher Special Consumption Tax increases product prices, making these goods highly profitable targets for smuggling. Can we effectively control this situation?

If not, the policy could backfire, with smuggled alcohol and beer flooding the market while the state fails to collect taxes from these products. VNS

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

.jfif) Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

.jpg) Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion

Opinion