Economy

Economy

Several sections of the Hồ Chí Minh Highway to be upgraded by 2030

1.

According to data from the General Department of Việt Nam Customs, Việt Nam’s trade deficit with other members of the Association of South East Asian Nations has been widening relentlessly in recent years, going up from US$3.2 billion in 2013 to $4 billion in 2014 and $5.5 billion last year.

|

| Thailand imported sandals at a shop in HCM City. The deficit with Thailand alone during this period was $3.3 billion. — Photo cafef.vn |

by Thiên Lý

According to data from the General Department of Việt Nam Customs, Việt Nam’s trade deficit with other members of the Association of South East Asian Nations has been widening relentlessly in recent years, going up from US$3.2 billion in 2013 to $4 billion in 2014 and $5.5 billion last year.

It climbed to $4.5 billion in the first nine months of this year.

The deficit with Thailand alone during this period was $3.3 billion. It was $1.4 billion with Malaysia and $1.8 billion with Singapore.

Analysts attributed Việt Nam’s increasing trade deficit to the free trade agreements it has signed.

For instance, the import of automobiles from Thailand increased consistently in the last seven months, as 18,837 units worth more than $343 million were shipped to the country. This made Thailand Việt Nam’s leading automobile exporter.

Preferential import tariffs under Việt Nam’s ASEAN Trade in Goods Agreement commitments caused the sharp increase in car imports from Thailand.

Under the agreement, the import tax on automobiles from ASEAN members – Myanmar, the Philippines, Malaysia, Thailand, Singapore, Laos, Indonesia, Cambodia and Brunei besides Việt Nam – will fall from 50 per cent to 40 per cent by 2016, to 30 per cent by 2017 and zero per cent by 2018.

The customs department figures show that Thailand was followed by South Korea, which shipped 3,560 cars to Việt Nam, and China with 2,260 units.

As for South Korea, besides a trade deal between it and ASEAN, the Việt Nam-South Korea Free Trade Agreement (VKFTA), which took effect last December, has also helped boost its exports to Việt Nam, especially of machinery and equipment and raw materials by causing import tariffs to be cut sharply, even to zero in some cases, with immediate effect.

The analysts also pointed out some other reasons for Việt Nam’s big trade deficit, one of which is the proliferation of major foreign-invested projects, especially by Chinese companies in the country.

Việt Nam’s imports comprise of three main categories: capital goods, mainly machinery and equipment (accounting for 30 per cent of imports), intermediate goods (60 per cent) and consumer goods (10 per cent).

A majority of capital and intermediate goods imported is for projects won by Chinese investors in this country.

China is also the biggest provider of capital and immediate goods to Việt Nam.

Besides, the domestic industrial sector’s low competitiveness, particularly in support industries, forces many Vietnamese private and even State-owned enterprises to import machinery and equipment from South Kroea, ASEAN members and, especially, China.

Việt Nam’s deeper and deeper integration into the global supply chain has also encouraged its businesses to import intermediate goods and assemble them into final products for exporting to other markets like the US and Europe.

The analysts’ biggest concern now is that while goods from ASEAN members, China and South Korea are flooding into the market, Vietnamese firms are still busy themselves with seeking ways to export their products to those countries .

Converting banks’ bad debts into equity: can it work?

The State Bank of Việt Nam is said to be considering a mechanism that will enable banks to convert their bad debts into equity in their debtor companies.

According to a draft circular, the banks will be allowed to convert bad debts classified in the fifth group (potentially irrecoverable debt) and those already settled thanks to risk provisioning.

Loans are classified into five groups, the four others being standard debts, debts needing special attention, subprime debts, and doubtful debts.

Another condition is that the total bad debts eligible for conversion must not exceed 40 per cent of the prescribed capital plus reserve fund of the bank and 60 per cent in case of a finance company.

The involved credit institutions will also be asked to ensure the capital adequacy ratio (CAR) as regulated before and afer converting their bad debts into the contributed capital or shares (equity) at their debtor businesses.

According to the HCM City Securities Joint Stock Company, non-performing loans or bad debts in the domestic banking sector now account for 9.2 per cent of GDP by late June. As of the end of August the bad debts ratio had come down to 2.66 per cent as against a target of 3 per cent.

By the the end of the second quarter the Việt Nam Asset Management Company had VNĐ217 trillion worth of bad debts it had bought from banks, or equivalent to 5.75 per cent of GDP.

Though bad debts at most local banks now stand at below the 3 per cent target, they remain one of the biggest problems facing the banking sector and also the economy, forcing the central bank to explore ways to resolve the issue.

Converting bad debts into equity is believed to be one of the most effective methods for lenders to partly settle their bad debts.

Experts say this has its advantages.

Now bad debts could be settled within months rather than the years it takes an asset management company to collect them.

It would enable debtor companies to clean up their balance sheets and borrow afresh to invest in production and business activities. Many of them are moribund because they lack resources to continue doing business.

Banks too will benefit if they can lend again to many companies that are now not considered creditworthy.

But surprisingly, the draft circular has been rejected by many banking experts who flagged concerns about “heaping new debts on old ones” and banks into non-core businesses.

The debtors operate in various sectors such as real estate, steel production, construction, rice farming, etc, and any equity holding in them could see banks forced into managing them, they warned.

Besides, it could also require the banks to pump more money into the debtor companies to resuscitate them, resulting in them throwing good money after bad.

The experts also dismiss it as “old wine in a new bottle” since the banks would still not recover the debts, merely take them off their balance sheets with some creative accounting

Finally, the Ministry of Finance’s Debt and Asset Trading Company has already tried this method when restructuring sick companies, and the results have been nothing to write home about. -- VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

MobiFone Telecommunications Corporation earned more than VNĐ2.50 trillion (US$111.11 million) in after-tax profit in the first half of this year, down two per cent over the same period last year.

Economy

Economy

Shares appear set to remain steady this week as investors remain cautious on lack of positive business news in both domestic and international markets, securities companies and analysts said.

Economy

Economy

Việt Nam’s agricultural production has gradually entered the global supply chain, according to the Việt Nam Logistics Institute (VLI).

Economy

Economy

The Việt Nam Information Technology Outsourcing Alliance (VNITO) and the non-profit Japan Information Service Innovation Partners Association (JASIPA) last Friday signed a memorandum of understanding to promote business co-operation and leverage the strengths of both sides for sustainable development of their members.

Economy

Economy

New foreign direct investment (FDI) registered in the 10 months of this year decreased by 1.3 per cent year-on-year to US$12.3 billion despite an annual rise of 25 per cent in the number of projects.

Economy

Economy

Vietnamese small and medium-sized enterprises (SMEs) are encouraged to promote brand building and e-commerce development to enhance competitiveness at a workshop on e-commerce yesterday in Cần Thơ City.

Economy

Economy

The Vietnamese Government has issued a resolution approving the extension of its rice trade agreement with the Philippine Government.

Economy

Economy

Vietnam-based online video startup Big Cat Entertainment Co Ltd has sold a major stake to Asia Innovations Group (AIG), a Chinese mobile internet company developing social and entertainment products.

Economy

Economy

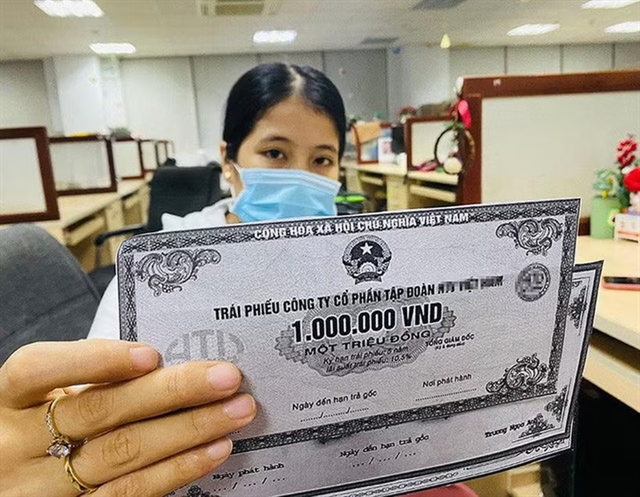

Deputy Minister of Finance Trần Văn Hiếu urged measures to boost the bond market at the third general assembly of the Việt Nam Bond Market Association.