Economy

Economy

Keeping coastal tradition alive

1.

|

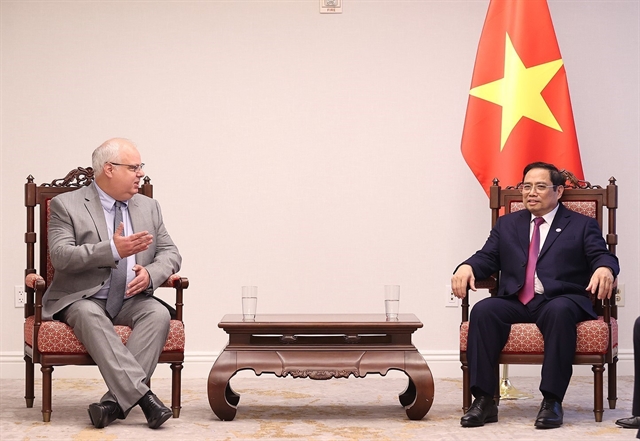

| A view of HCM City. Many banks have temporarily ceased lending to the property sector. —Photo vneconomy.vn |

Compiled by Thiên Lý

Deputy Governor of the State Bank of Việt Nam, Đào Minh Tú, announced at the Government’s March press conference that credit growth in the first quarter of the year had been 5.04 per cent, much higher than the 2.16 per cent rise in the same period last year.

He described it as a “quite positive result” that showed the economy had made a significant recovery with people’s lives and businesses returning to normal thanks to the Government’s effective measures against the COVID-19 pandemic.

According to a report by the SBV’s HCM City office, credit growth in the country’s main economic hub was estimated at 3.65 per cent in the first quarter.

The positive performance has encouraged many banks to set high goals for the full year.

At its annual general meeting on March 16, VIB approved a growth target of 30 per cent, much higher than the cap of 14 per cent set by the central bank for the overall banking sector.

Viet Capital Bank expects to achieve credit growth of 15 per cent this year.

State-owned lenders Vietcombank and Vietinbank have also set high targets of 12 and 14 per cent.

Explaining the reason for the high credit growth since the beginning of the year, analysts said both private and State-owned banks stepped up lending to help businesses across the board recover from the worst impacts of the pandemic and reconnect disrupted supply chains.

Their strong financial support came mainly in the form of preferential loan packages.

Banking analyst Dr NguyễnTrí Hiếu said Việt Nam’s economy had shown great resilience while consumer demand had recovered well, creating opportunities for enterprises to expand their business and production activities.

So enterprises’ demand of funding increased sharply, he said.

Credit restriction

But some analysts said credit did not actually flow into areas that would boost the economy.

They pointed out that while the credit growth was so high the country’s demand still recovered slowly.

Lã Giang Trung, general director of Passion Investment, told Đầu Tư newspaper that enterprises remained mired in difficulties but yet the banking sector credit growth was high.

It just meant loans were used mainly for investment in assets like property and securities and not for production and other business activities, he said.

Techcombank was among the biggest lenders to the property sector last year, both for development and mortgages.

In the first nine months of last year it lent VNĐ130 trillion (US$5.7 billion) to developers, 50 per cent higher than in the same period of 2020 and accounting for 40 per cent of its total loans, rising to an estimated 75 per cent if mortgages are included.

Other major lenders to the sector were VPBank, VIB, MBBank, TPBank, and MSB.

Economist Dr Cấn Văn Lực said in the past lending interest rates were low, which encouraged people to borrow money to buy, repair, build, and even invest in real estate.

He said total outstanding loans to the property sector now were estimated at VNĐ2,000 trillion, accounting for 20 per cent of overall loans.

But the actual rate might be much higher.

Lending to the property sector last year increased by 12 per cent, with mortgages and loans to finance repairs rising by 15-16 per cent and loans to developers by 6-7 per cent.

On March 18 the SBV issued an action programme based on the Government’s Resolution No.11/NQ-CP dated January 30 under which it required banks not to ease lending regulations and to refrain from funding real estate and securities investment and build-operate-transfer and build-transfer transport projects.

Following this, many banks have temporarily ceased lending to the property sector.

Sacombank has for instance instructed all its branches to focus on lending to certain production and priority sectors such as supporting industries, small and medium-sized enterprises, high-tech companies, trade, services, logistics, agriculture, rural development, and exports.

It has directed them not to fund the real estate sector until the end of June.

Techcombank has decided to stop mortgages from March 25 and said would consider resumption in the following quarters.

Many other lenders also plan to control their credit flows.

At the VIB annual general meeting this year, vice chairman Đặng Văn Sơn said the bank would minimize real estate loans and give priority to people who want to buy, build or repair houses for living.

Developers and property buyers wonder what the impact of this tightening will be.

Many say they are afraid it would be negative since most real estate players use debts to buy assets.

The CEO of a real estate firm in HCM City’s Tân Bình District said the tightening of real estate lending would badly affect the market since even financially strong firms like his also need financial support from banks.

Big companies might be able to raise funds from other sources but not smaller ones, he said.

Some analysts point out that the industry expects the property market to grow robustly this year and do not want to miss out on opportunities due to lack of funding from banks.

Economist Dr Đinh Thế Hiển said developers building now or with products on sale would also be affected since buyers would find it difficult to take out mortgages.

But some analysts point out that people looking to buy houses for living will not have any difficulty in getting loans.

The Bank of Agriculture and rural Development, for instance, has only cut lending to real estate speculators and still provides loans to customers who want to buy or repair houses to live in.

Ngô Đức Sơn, director of DRH Holdings, agreed that stringent lending regulations are necessary since they would make the market less risky and speculative. — VNS

Economy

.jpg) Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

The State Securities Commission (SSC) is closely monitoring the developments of the economic - political situation, assessing the influence on Việt Nam's stock market in order to promptly take appropriate solutions aimed at stabilising the domestic stock market, said a representative of SSC.

Economy

Economy

The Vietnam International Premium Products Fair will be held again in HCM City after being delayed due to the COVID-19 pandemic.

Economy

Economy

Markets experienced the worst performance since March 2020 last week due to strong selling pressure. Experts said that with the current conditions, downside risk is still dominating the market.

Economy

Economy

Results of co-operation between the Ministries of Planning and Investment, as well as the Cooperation Committees of Laos and Việt Nam in recent years have made important contributions to the development of the two countries’ relations, Lao Minister of Planning and Investment Khamjane Vongxa said on Friday.

Economy

Economy

Economy

Economy

A consulting session on exporting dragon fruits to Australia and New Zealand was organised in the southern province of Long An on Thursday.

Economy

Economy

Prime Minister Phạm Minh Chính met with President and Chief Executive Officer of Murphy Oil Corporation Roger Jenkins in Washington D.C on May 13 afternoon (local time) as part of his trip to the US.

Economy

Economy