Economy

Economy

PM urges comprehensive legal corridor to promote national digital transformation

1.

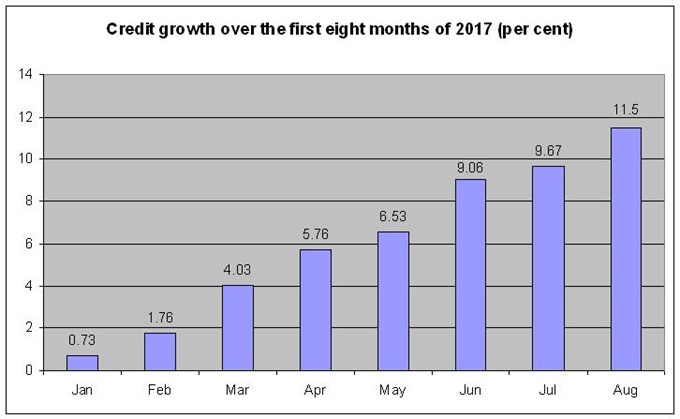

Credit growth rate in the first eight months of 2017 has been estimated at 11.5 per cent compared to the end of 2016, the National Financial Supervisory Commission (NFSC) reported.

|

| Source: National Financial Supervisory Commission. — VNS Infographic Ngọc Bích |

HÀ NỘI — Credit growth rate in the first eight months of 2017 has been estimated at 11.5 per cent compared to the end of 2016, the National Financial Supervisory Commission (NFSC) reported.

As per the report, this figure is 1.3 percentage points higher than the first eight months of 2016.

Short-term loans rose by 14.1 per cent, accounting for 45.9 per cent of total outstanding loans, while medium- and long-term lending grew by 8.8 per cent, making up 54.1 per cent, the NFSC report said.

The proportion of credit in đồng in total outstanding loans rose by 11 percentage points to 91 per cent. Notably, the credit in foreign currency jumped by 11.5 per cent compared to the same period last year. In 2016, the growth rate of foreign currency credits in the first eight months was only 1.7 per cent.

From January to August, the banking system’s deposit growth rate was 9 per cent; the figure in the corresponding period last year was 11.4 per cent.

In terms of interest rates, the State Bank of Việt Nam (SBV) said the average interest rates for short-term loans stood at 6.8 to 9 per cent per year, and for medium- and long-term loans at 9.3 to 11 per cent.

Lawyer Bùi Quang Tín, CEO of BizLight Business School, said there are several factors that could help reduce interest rates or stabilise them in the coming months. One factor is abundant liquidity in commercial banks, which could help satisfy the spike in credit demand in the last quarter of the year.

Also, the central bank has been continuously buying the US dollar to increase the foreign reserve; inflation is being controlled actively; and inter-bank interest rates have dropped to the lowest level since the beginning of 2017, Tín said.

However, financial and banking expert Nguyễn Trí Hiếu said reducing interest rates by a further 0.5 percentage points is only feasible if the SBV increases buying bonds from commercial banks to supply more money to the market. Since the beginning of the year, credit growth has been higher than deposit growth, so without the SBV’s support, commercial banks would probably have to increase deposit interest rates to raise more capital.

Hiếu warned that bond buying, however, might push up inflation.

He also stressed the importance of settling bad debts to further reduce lending interest rates, as currently, banks have to set aside large provisions for bad debts, which raises their costs.

The annual interest rates for deposits ranging from one to below six months averaged at 4.5 to 5.4 per cent; those with terms between six and 12 months at 5.4 to 6.5 per cent, and for over 12 months at 6.4 to 7.2 per cent.

The total post-tax profit of credit institutions in the first seven months of 2017 touched VNĐ41 trillion (US$1.8 billion), a 60 per cent surge on the same period last year, mostly thanks to lending and services provision activities. As of June 30, bad debts of credit institutions amounted to VNĐ157 trillion, a 21.5 per cent rise compared to the end of 2016, accounting for 2.9 per cent of total outstanding loans. — VNS

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Economy

Hà Nội’s economy has expanded since the beginning of this year with steady growth recorded in all key sectors of industry, trade, tourism and services and agriculture, reported the municipal People’s Committee.

Economy

Economy

It’s expected to be a strong September on the local stock market, as investors are maintaining confidence after positive economic data in August and a period of prolonged net buying by foreign traders.

Economy

Economy

A new full-moon season starts in one month and confectioneries nationwide are ready with many kinds of mooncakes with new flavours.

Economy

Economy

Foreign online travel agencies have been dominating the online tourism market in Việt Nam.

Economy

Economy

The Ministry of Finance has held a meeting to introduce changes in the list of Việt Nam’s export and import goods as per Circular No 65/2017 / TT-BTC.

Economy

Economy

The State Bank of Việt Nam (SBV) has issued a draft amendment updating a new circular regulating capital ratios for the operation of credit institutions and foreign bank branches.

Economy

Economy

The Hà Nội Stock Exchange (HNX) will assess and honour the top 30 listed companies for best corporate governance in November during its annual convention for listed businesses.

Economy

Economy

After a new trade deal, a Vietnamese company are hoping to add a new country to their roster of important trading partners: Armenia.

Economy

Economy

The budget carrier Jetstar Pacific Airlines officially launched direct air routes linking Hà Nội, Đà Nẵng City and Japan’s Osaka City last week.